What Did the Inflation Reduction Act (IRA) Change?

And how does it affect value and evidence strategies for biopharma

TLDR

The IRA is compressing commercial value for high-spend Medicare drugs, and changing how manufacturers approach launch pricing, evidence generation, and portfolio planning.

Impact on biopharma value and evidence strategies:

Greater risk of underpricing at launch

Medicare exposure a bigger factor for pipeline decisions

More reliance on real-world evidence to prove differentiation

Ripple effects from competitor negotiations

Small molecules may face more pressure than biologics

Indication sequencing and expansion may change, especially in oncology

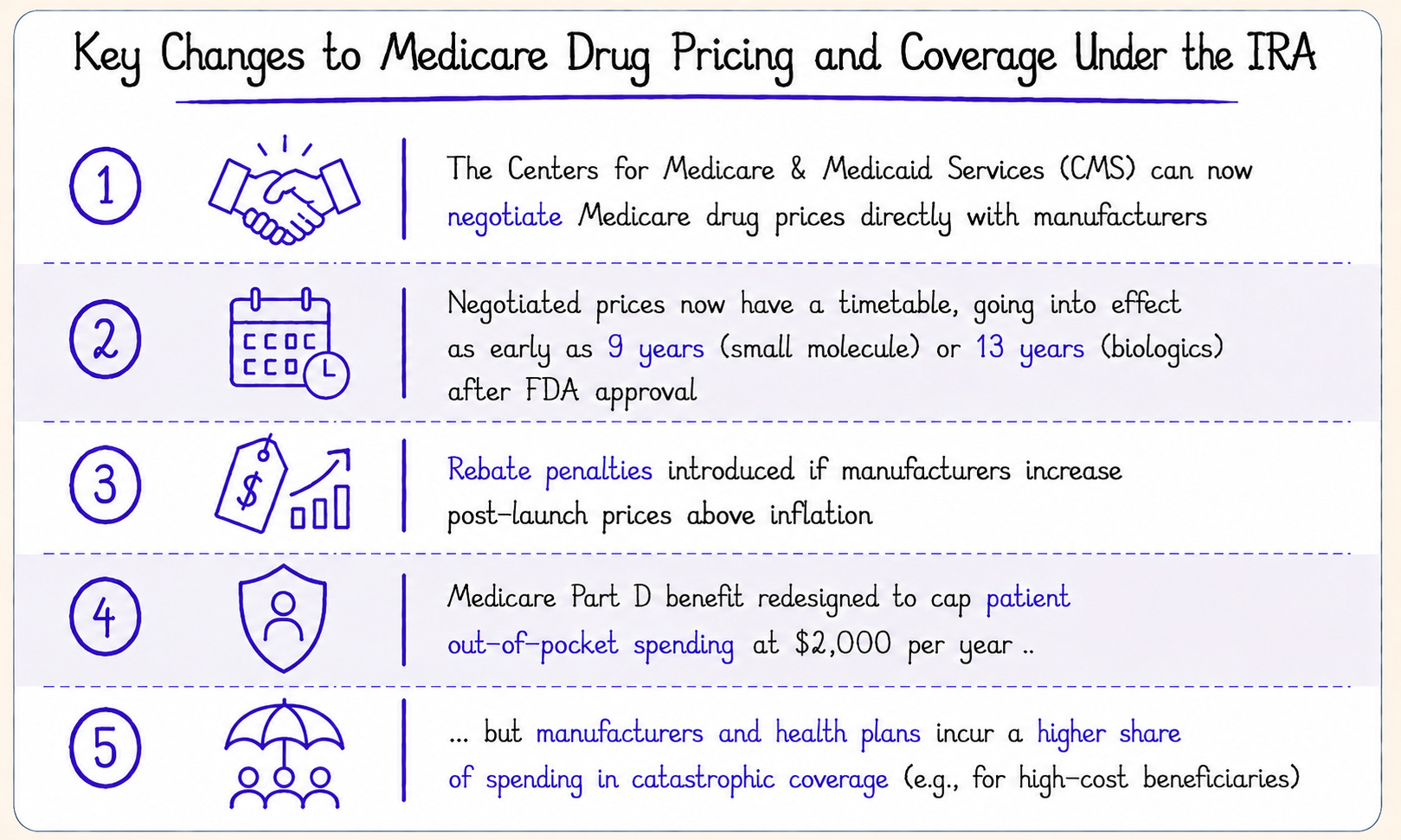

The Inflation Reduction Act (IRA)

The IRA has introduced one of the biggest shifts in decades for US biopharma.

Before the IRA, price erosion in Medicare was driven by market forces: competition, generic entry, and payer negotiations. Manufacturers expected prices to decline over time, but timing and magnitude varied widely across drugs.

For the first time, the IRA allowed CMS to negotiate Medicare prices directly with manufacturers, resulting in Maximum Fair Prices (MFPs) for selected drugs.

The IRA also introduced other changes, including:

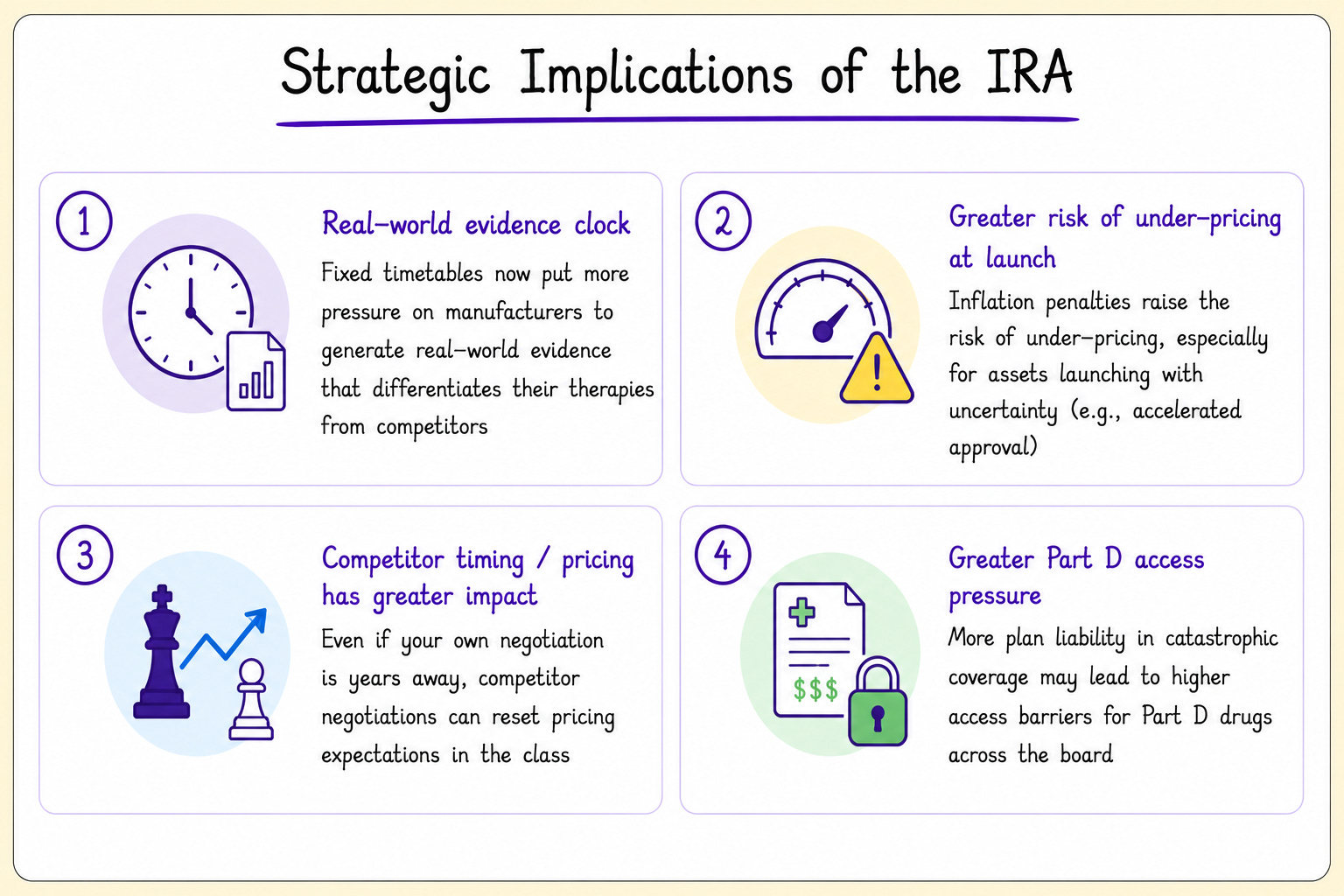

Strategic Implications of the IRA

Early negotiation cycles have shown that CMS is focused on drugs with high Medicare spending and whether drugs are differentiated vs. therapeutic alternatives.

Because head-to-head trials between competitors are often unavailable, manufacturers will increasingly turn to real-world evidence to prove differentiation.

Additionally, manufacturers face new risks if drugs are underpriced at launch, if competitors face IRA negotiations, and if Part D plans increase utilization management and access barriers.

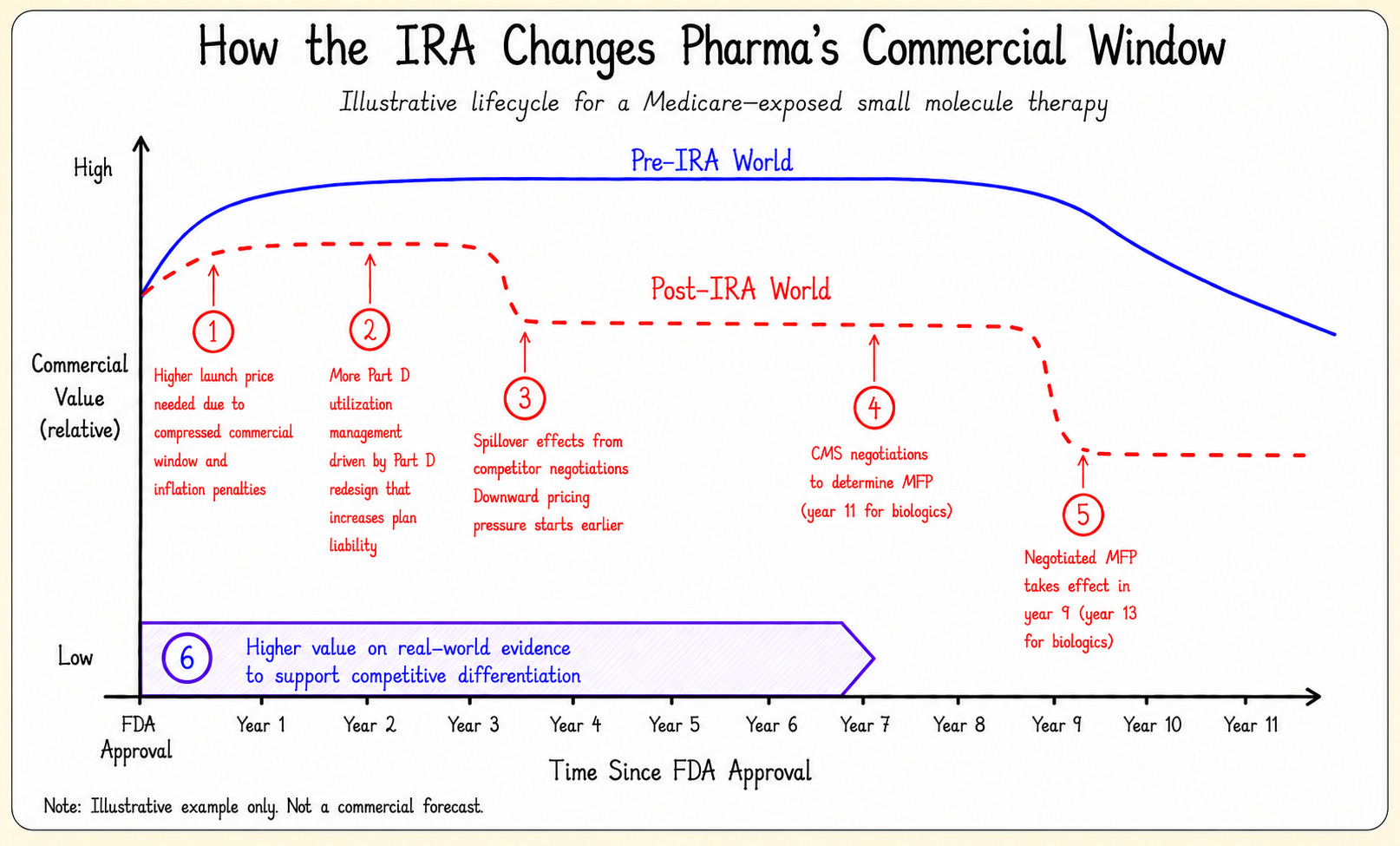

Hypothetical Impact for a Small-Molecule Drug

A hypothetical example is shown below for “Drug X,” a small-molecule drug covered under the Part D benefit, to illustrate how these changes might impact commercial value in Medicare.

In early years, more aggressive utilization management by Part D plans may lead to lower sales volumes. By year 3, a competitor’s negotiation could also put downward pricing pressure on Drug X.

By year 7, Drug X might have enough Medicare spend to be selected for negotiation. The negotiated MFP would take effect in year 9. Part D plans would be required to cover Drug X, but coverage would not eliminate utilization management.

How Does the IRA Change Manufacturer Strategy?

Much discussion of the IRA has focused on CMS’ new ability to negotiate prices. But price negotiations are only one piece of the larger puzzle.

In fact, the IRA impacts many upstream decisions, such as asset prioritization, launch pricing, post-launch evidence generation, and indication sequencing.

1. Portfolio prioritization and scenario planning

The IRA compresses commercial value for Medicare drugs, making Medicare exposure a bigger factor in portfolio planning. Some clinically promising assets may look less attractive once negotiated prices, competitor timing, and Medicare mix are modeled.

2. Competitor timing and differentiation

Competitor negotiations are now an important factor. If a competitor launches ahead of you, its negotiated MFP may accelerate Medicare pricing pressure, with potential spillover into commercial books of business. Strong evidence of differentiation may help manufacturers defend against these pressures.

3. Launch pricing

Inflation penalties give manufacturers less room to raise prices after launch, increasing the risk of underpricing. The challenge is setting a launch price that reflects a drug’s full value while also accounting for uncertainty, payer pushback, and compressed commercial timelines.

4. Evidence generation

CMS negotiations have focused on how drugs compare with therapeutic alternatives. Because head-to-head trials are often unavailable, manufacturers will rely more on real-world evidence to prove differentiation.

5. Indication sequencing and expansion

The IRA may change how manufacturers sequence indications, especially in oncology where drugs often launch first in smaller, later-line populations before expanding.

Because the negotiation clock starts after first FDA approval, smaller initial launches may leave less time to capture value from larger follow-on indications. That could make manufacturers more selective about initial approvals and post-launch expansions.